Sustainability reporting vs sustainability disclosure — what's the difference?

If you Google these two terms, you'll quickly get the impression that they mean roughly the same thing. Many people use them interchangeably, and it's easy to see why — they sound nearly identical and are clearly about the same subject. But there are real differences, and they matter for you.

.png&w=3840&q=75)

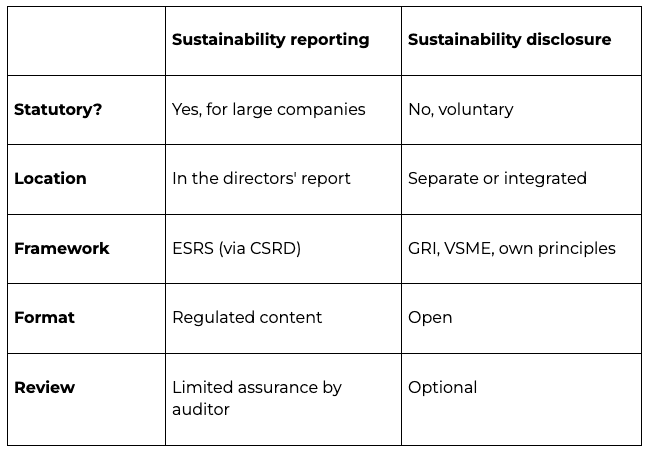

The short version: sustainability reporting is the legal requirement. Sustainability disclosure is something you do voluntarily. They are related, but not the same thing.

Below we untangle the concepts properly — without unnecessary consultant jargon.

Sustainability reporting — the statutory requirement

Sustainability reporting is the term used in legislation. New provisions in the Annual Accounts Act came into force on 1 July 2024, and the sustainability report must be included in the annual report as a separate section of the directors' report. It is therefore not a standalone brochure or a voluntary summary — it is a legal document with specified content.

The basis is the EU's CSRD (Corporate Sustainability Reporting Directive), which in Sweden has been implemented through amendments to the Annual Accounts Act. The directive replaces the previous NFRD directive and aims, among other things, to steer capital towards sustainable investments, facilitate the management of financial risks related to climate and the environment, and make sustainability information comparable across companies.

Which companies must produce a sustainability report?

In December 2025, the EU voted through significantly raised threshold values as part of the so-called Omnibus package. The proposal means that the obligation to produce a sustainability report will be limited to companies with more than 1,000 employees and an annual turnover of at least €450 million — both conditions must be met. The directive entered into force in March 2026 and must now be implemented into Swedish law, which is expected to happen during 2026. Until the legislative change is in place, current Swedish rules apply.

What must the report contain?

This is governed by ESRS (European Sustainability Reporting Standards), the European sustainability reporting standards developed by the European Commission under CSRD. The report must contain information covering environment, social conditions, and corporate governance — collectively referred to as ESG. This covers everything from climate emissions and energy use to staffing matters, human rights, and anti-corruption.

The report must be reviewed by an auditor. This is not a full audit, however, but what is known as a limited assurance review, in which the auditor expresses a view with limited certainty that the information is reasonable and prepared in accordance with the regulatory framework.

Sustainability disclosure — the voluntary document

Sustainability disclosure is a broader and more open-ended term. It is not regulated by law. A sustainability disclosure can be prepared voluntarily, in accordance with a recognised framework such as ESRS or VSME, or according to the company's own internally developed accounting principles. There is therefore no law requiring you to produce a sustainability disclosure — but there is an abundance of standards and frameworks to help you do so in a structured way if you choose to.

What frameworks exist for voluntary sustainability disclosure?

GRI (Global Reporting Initiative) is the framework followed by the largest number of voluntary sustainability disclosures globally. It is an international standards body that helps companies communicate their sustainability work through an established system of guidelines and performance indicators. VSME is a newer framework developed specifically for small and medium-sized enterprises — more on that below.

A sustainability disclosure can be called almost anything: an environmental report, a CSR report, a sustainability statement, or a sustainability narrative. What matters is the content, not what you call the document. It can be published as part of the annual report, in a separate report, as a page on the website, or as a PDF. The format is open.

Since there are no statutory requirements for content and format, a sustainability disclosure can take many different forms — one page or a hundred, focused solely on climate or broader ESG issues, with or without third-party review. It is precisely that freedom that makes the concept harder to grasp, but also more adaptable for a small business that wants to communicate its sustainability work without navigating complex legislation.

What is the relationship between the two terms?

They are connected, but not synonymous — and it can be worth keeping them apart.

Think of it this way: sustainability reporting is the legal requirement covering what you must disclose and where it must be placed in your annual report. Sustainability disclosure is the broader document — often voluntary and framework-based — that describes your entire sustainability work, including things the legislation does not require but that your stakeholders still want to know.

It does happen that a company required by law to produce a sustainability report also chooses to produce a sustainability disclosure in parallel, in order to communicate more than the statutory format allows. The sustainability report goes in the directors' report. The sustainability disclosure can be published separately — on the website, as part of a communications package, or in what is known as a front section of the annual report document, meaning a section that precedes the statutory parts.

The difference can be summarised roughly as follows: sustainability disclosure is the larger umbrella concept that encompasses everything sustainability-related you choose to communicate. The sustainability report is a specific statutory section with regulated content.

In practice, the terms are still used interchangeably in everyday conversation, in the media, and sometimes even in professional contexts. That makes it all the more important that you as a business owner know what you mean when you use them — and what your customer, bank, or auditor means when they make demands.

What should a small business care about?

The short answer is: probably both, but for different reasons.

You may not currently meet the conditions for statutory reporting — more than 250 employees, high turnover, large balance sheet total. But you are still under pressure, and that pressure increases year by year.

Banks ask about sustainability when assessing credit applications. Larger customers — who are themselves required to produce a sustainability report under CSRD — must disclose their emissions across the entire value chain, which means they need sustainability data from their suppliers. That is, from you. Procuring authorities are including sustainability requirements in more and more tenders. And investors, regardless of the size of your business, are beginning to ask questions that were previously the preserve of large listed companies.

The Omnibus package means that the formal requirements to produce a sustainability report now look set to apply to significantly fewer companies — with new thresholds of 1,000 employees and €450 million in turnover, the vast majority of SMEs fall outside the scope. But that does not change the fact that customers, banks, and public procurers are imposing their own sustainability information requirements — requirements that do not follow the thresholds set by legislation. The pressure comes from below and above, regardless of what the law says.

This means that even if your company is not legally required to produce a sustainability report, there are strong business reasons to have a grip on your numbers and be able to present them credibly. A voluntary sustainability disclosure based on a recognised framework gives you exactly that: a standardised way to gather and present your sustainability information that your customers, banks, and partners can actually understand and use.

What is VSME and why is it relevant for you as an SME?

VSME — Voluntary Sustainability Reporting Standard for SMEs — is a framework developed specifically for small and medium-sized enterprises. It was launched by EFRAG (European Financial Reporting Advisory Group), the same body that developed ESRS for large companies, and is designed to be manageable without a dedicated sustainability team.

VSME is voluntary, but it is not arbitrary. It follows the same underlying logic as CSRD and ESRS and is compatible with the requirements that large customers impose when collecting sustainability data from their suppliers. This means that a VSME disclosure can actually answer the questions your major customer or bank asks you to fill in — without you having to reinvent the wheel every time.

The framework is divided into two modules: a basic section covering the most important key figures on climate, energy, waste, and core social issues, and an extended section for those who want or need to go deeper. You choose the level based on your company's size and the requirements actually being placed on you.

For a small or medium-sized business, VSME is a practical way to stay one step ahead — before requirements are potentially tightened further and before customers start asking questions you can't answer.

How do you collect sustainability data in practice?

This is where many people get stuck. It doesn't matter which term you use or which framework you choose if you don't have access to actual data.

Sustainability data for a small business is largely about carbon emissions — and carbon emissions are largely about what you buy. Travel, energy, purchases of goods and services. The majority of a small company's climate impact shows up in supplier invoices.

The traditional way to collect this information is manually: export data from the accounting system, match against emissions factors, calculate, double-check, update when something changes. It takes time, requires some knowledge, and still often leads to uncertain figures because the method is so dependent on manual judgements.

A more modern approach is to use a tool that does the job automatically — pulling data directly from invoices and receipts, calculating emissions on an ongoing basis, and structuring the information so it is ready to use in a sustainability disclosure. That is precisely the logic GoClimate is built on: that sustainability disclosure should be able to run itself, without you having to spend significant time chasing figures.

Summary

In short: sustainability reporting is what the law requires. Sustainability disclosure is what you choose to do — and often what actually builds trust with customers, banks, and partners.

For you as an SME, the voluntary sustainability disclosure is often the more relevant place to start. That is where you can begin to control the narrative, pull your numbers together, and demonstrate that you take sustainability seriously — long before the legislator comes knocking.

Ready to take the first step?

GoClimate automatically collects sustainability data from your invoices and receipts — so you can produce a sustainability disclosure in line with VSME without spending time on manual data collection. The result is a disclosure that holds up to scrutiny, that your customers understand, and that looks after itself.

Sources

- [1] FAR – Hållbarhetsrapportering och hållbarhetsredovisning

- [2] Finansinspektionen – Hållbarhetsrapportering (NFRD/CSRD)

- [3] Revideco – Hållbarhetsredovisning eller hållbarhetsrapport?

- [4] U&We – Senaste nytt om Omnibus, CSRD och CSDDD – december 2025

- [5] FAR – Vad är Omnibus?

- [6] PwC – Hållbarhetsrapportering – vilka upplysningar behövs?

- [7] Finansinspektionen / EFRAG – VSME-standard

Want to go from knowledge to action?

See how GoClimate turns your accounting into a report you can act on.