Scopes according to the GHG-protocol

Updated at 2026-05-07

Let's break down the different types of emissions related to a company's activities according to the GHG Protocol — scope 1, 2 and 3 — in a way that's easy to understand! The framework is today the dominant standard for climate reporting globally, and underpins most sustainability reporting requirements placed on companies today. Simply put, Scope 1 covers the emissions a company directly produces, Scope 2 concerns emissions from the energy it uses, and Scope 3 includes all other emissions related to its activities, from the goods it purchases to the services it uses.

Why does the scope structure matter for your company?

The GHG Protocol's scope structure is not just a way to categorize emissions — it's a strategic tool. By understanding where your emissions actually arise, you can make better decisions about where action will have the greatest impact, and communicate this credibly to customers, investors and business partners.

A growing number of sustainability reporting requirements — from the EU's Corporate Sustainability Reporting Directive (CSRD) to the voluntary VSME standard for smaller companies — are built on the GHG Protocol's framework. This means that a basic understanding of scope 1, 2 and 3 is a prerequisite for being able to meet these requirements, whether voluntarily or due to legal obligation.

Want to calculate scope 1, 2 and 3 fully automatically and cost-effectively? Book a demo!

Scope 1 – Direct emissions

According to the GHG Protocol, Scope 1 covers direct emissions — that is, emissions that come directly from sources owned or controlled by a company. Think of it as the exhaust from the cars in a company's fleet, provided those cars run on fossil fuels rather than electricity.

What counts as Scope 1 emissions?

The most common examples are combustion of fossil fuels in own vehicles, such as a fleet running on petrol or diesel, heating of premises with oil or natural gas, industrial processes that emit greenhouse gases directly — for example manufacturing or chemical handling — and refrigerants leaking from air conditioning or cooling units (so-called fluorinated gases, or F-gases).

For many service companies and office-based operations, Scope 1 emissions are limited — perhaps only emissions from a leased vehicle fleet. For manufacturing and transport companies, however, they can constitute a significant share of the total carbon footprint.

How is Scope 1 calculated?

The calculation is typically based on actual fuel consumption multiplied by emission factors — standardized values indicating how many carbon dioxide equivalents (CO₂e) are generated per unit of fuel. For Swedish operations, the Swedish Environmental Protection Agency (Naturvårdsverket) publishes emission factors for direct combustion emissions, updated annually [1]. The IPCC provides default values (Tier I) used primarily as a fallback when national data is unavailable [2].

Scope 2 – Indirect emissions from purchased energy

Scope 2 concerns greenhouse gas emissions from the production of the energy a company uses — not from the operations themselves, but from the sites that generate the energy. The classic example is the power plant producing electricity for an office. According to the GHG Protocol, this is one of the three fundamental categories that organizations worldwide use in their climate reporting.

Scope 2 – more complex than it appears

Calculating Scope 2 emissions sounds straightforward: purchased electricity multiplied by the grid's emission factor. In practice, however, there are two different methods to choose between, and the choice significantly affects the result.

The market-based method takes into account whether a company has entered into agreements for renewable electricity, for example by purchasing Guarantees of Origin (GO certificates). If you buy certified hydropower or wind power, your Scope 2 can be reported as zero — even though physically you are connected to the same grid as everyone else.

The location-based method instead uses the average emissions of the grid you are connected to, regardless of which electricity you have purchased. The Swedish electricity mix is generally very low in emissions thanks to a large share of hydropower and nuclear power, but this varies.

Dual reporting is a requirement — not a recommendation

The GHG Protocol's Scope 2 Guidance has since 2015 required that both methods be reported for organizations operating in markets where supplier-specific emission factors are available [3]. CSRD and ESRS E1 have incorporated the same requirement for the companies covered by the directive [4]. This is therefore not an upcoming requirement — it already applies. It is also important to state which method is used, otherwise information from different companies cannot be compared.

In addition to electricity, Scope 2 also includes district heating, district cooling and steam purchased from external suppliers.

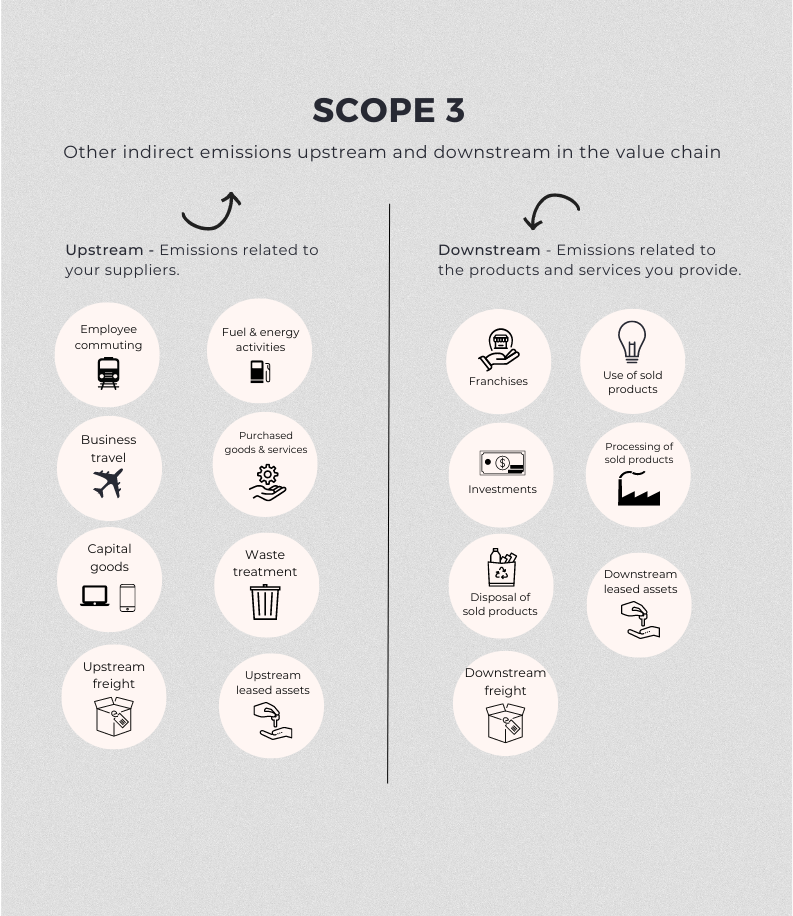

Scope 3 – All other indirect emissions

Scope 3 covers emissions from everything from the production of the products a company purchases from others, to the use and end-of-life treatment of its own products. If a company purchases products from a supplier, the greenhouse gas emissions from the manufacturing of those products are considered Scope 3. It is like looking at the full picture of a company's impact, from start to finish, across its entire value chain.

Scope 3 – the most difficult and most important category

Scope 3 is often by far the largest source of a company's climate impact — and the most difficult to measure. According to the GHG Protocol, Scope 3 is divided into 15 categories, split between upstream and downstream emissions [5]. Upstream (categories 1–8) refers to emissions in the supply chain before raw materials or services reach the reporting company. Downstream (categories 9–15) refers to emissions after the reporting company has delivered its product or service to the customer — including transport, storage, use and end-of-life treatment of sold products. To reduce their total greenhouse gas emissions, companies should actively work with this entire area.

Upstream emissions

Common upstream categories include purchased goods and services — i.e. emissions from suppliers' production of what you buy — as well as business travel such as flights, trains and hotels for employees, employee commuting, capital goods such as machinery, vehicles and equipment, and waste management arising from the company's own operations and handled by external parties (Category 5: Waste generated in operations) [6].

Downstream emissions

On the downstream side, this includes among other things emissions when customers use what you sell, as well as end-of-life treatment and waste management of the products you have sold after they have been used up by the customer (Category 12: End-of-life treatment of sold products) [6].

Why is Scope 3 so difficult?

It requires information and data from multiple parties outside the company's own operations — suppliers, customers and transport providers. Many of these organizations do not share emissions data, which means that industry averages and default values often need to be used. This means Scope 3 figures always contain a degree of uncertainty — but it is still better to have an estimate than no data at all.

Scope 3 and the supply chain

One of the most important consequences of Scope 3 reporting is that it makes dependencies in the supply chain visible. Organizations that previously focused solely on their own direct energy consumption are now compelled to ask questions of their suppliers: How are raw materials produced? How are they transported? What energy agreement do they have?

This drives active supplier engagement along the value chain — a collaboration to jointly reduce greenhouse gas emissions. The GHG Protocol specifically highlights this as a key strategy: working with suppliers to collect primary data and set shared reduction targets [5]. Large companies are already placing these demands on their subcontractors, and that trend is accelerating with CSRD.

Read about how AstraZeneca places requirements at the supplier level.

The link to double materiality assessment

The EU's sustainability reporting directive CSRD introduces the concept of double materiality — a requirement for companies to assess both how climate change affects them (financial materiality) and how they affect the climate (impact materiality). The scope structure is directly linked to impact materiality: which parts of the value chain have the highest emissions, and where do we have the greatest opportunity to make a difference?

By mapping their scope 1, 2 and 3 emissions, a company gains a factual basis for conducting a credible materiality assessment.

How do you get started with scope reporting?

For a small or medium-sized company, starting to report emissions can feel overwhelming. A practical approach is to take it step by step — according to the GHG Protocol, emissions are divided into three scopes, and it makes sense to work through them in order.

Start by mapping the company's direct and indirect emissions in Scope 1 and 2 — these are easier to quantify and require data that is often already available in the form of fuel receipts and electricity bills. Then identify the most important Scope 3 categories: which purchases dominate, and how do your employees travel? The final step is to simplify data collection. With the right tools, purchasing data, travel data and energy data can be collected and converted into emissions figures without manual work.

Calculate your emissions with GoClimate — fully automatically

GoClimate automatically collects data from your invoices and receipts and converts them into a complete sustainability report — including scope 1, 2 and 3. Book a demo today!

Related content

Here you can find articles and pages relevant to this subject.

- 1. Naturvårdsverket – Beräkna direkta utsläpp från förbränning.

- 2. Naturvårdsverket – Beräkning enligt GHG Protocol eller ISO-standard.

- 3. GHG Protocol – Scope 2 Guidance (2015).

- 4. GHG Protocol – Scope 2 Standard Development Plan (2024).

- 5. GHG Protocol – Corporate Value Chain (Scope 3) Standard.

- 6. GHG Protocol – Teknisk vägledning, Category 5 - Waste generated in operations.